Kicking the can down the road

It has been an eventful few weeks for the oil market since Trump's inauguration on January 20, and it seems this next week will be no different.

This week, we will closely follow the three oil market reports from the EIA (Tuesday), OPEC (Wednesday), and the IEA (Thursday). We will focus on how the three agencies assess the impact of tariffs on crude oil demand. This will also be the first EIA report to factor in the "drill baby drill" policy. So far, the EIA has maintained a modest estimate for growth in US oil production. Regarding OPEC, its report will be closely scrutinised to determine whether its forecasts align with OPEC+ plans to add more oil to the market.

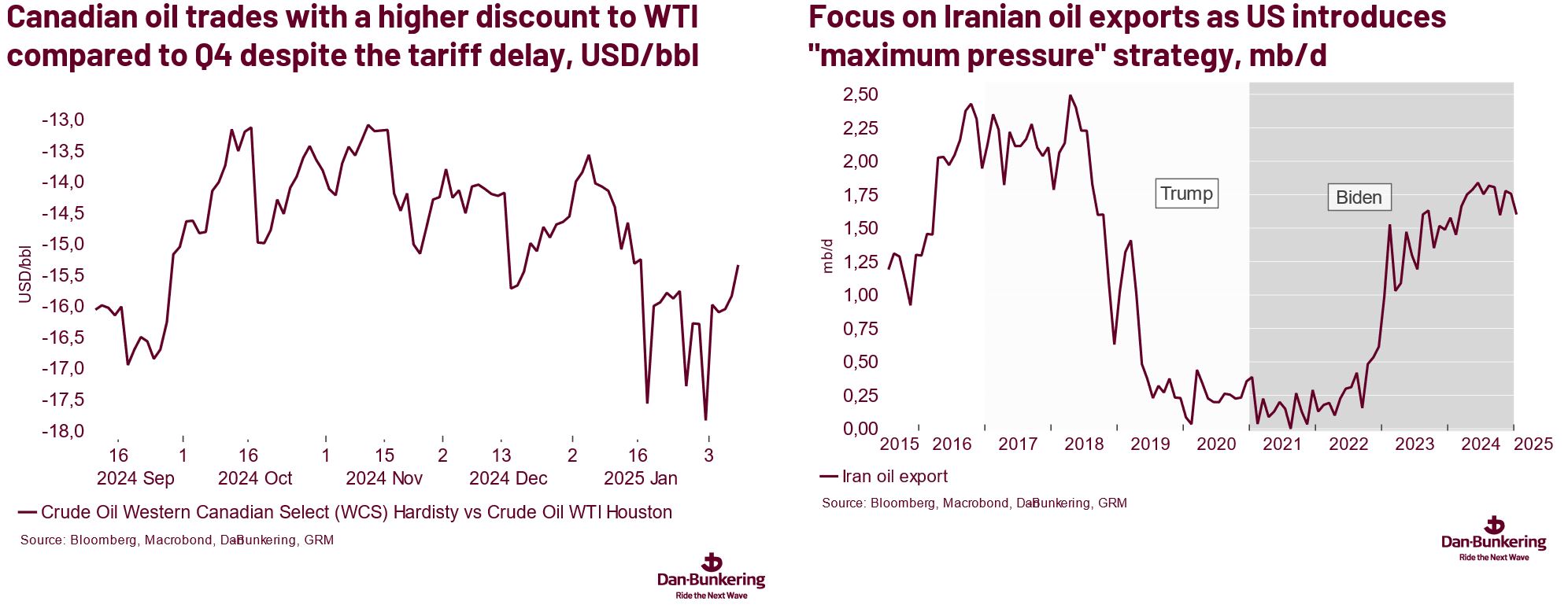

Last week, we examined two key events: the potential tariffs on Canada and Mexico and the OPEC+ meeting on February 3. Both events 'kicked the can down the road'